Maura Cutting, Berkshire Hathaway HomeServices Commonwealth Real EstatePhone: (781) 844-6078

Email: [email protected]

Email: [email protected]

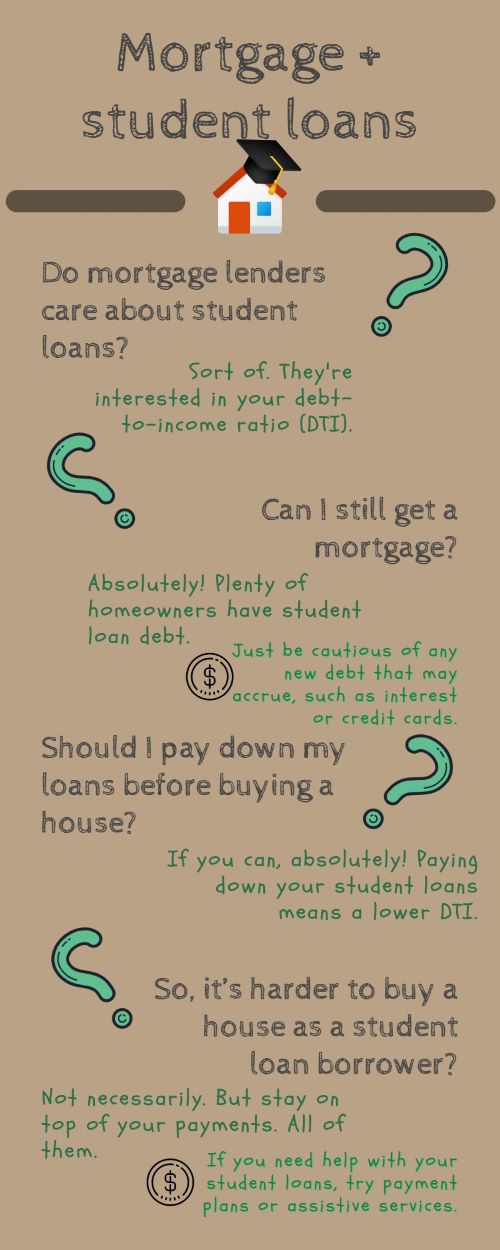

It's common for homeowners to have both mortgage and student loan payments simultaneously. But how does student debt affect your chances of getting a mortgage in the first place?

While lenders consider all debt obligations in loan approval, you can still buy a home while paying student loans.

Lenders consider your current financial obligations, including any outstanding loan balance, in your financial statement.

Your debt to income ratio, or DTI, measures your ability to make regular loan payments, so if your student loan payments skew your DTI too much, it could be a red flag to lenders.

While mortgage lenders consider your debt-to-income ratio for mortgage approval, you don't have to be completely debt free to get a mortgage. So, you can have student loan debt and still get a mortgage!

Student loan debt won't keep you from mortgage approval, but it can make it harder to qualify. If you have reliable income and a good payment history, it's not necessary to pay off your existing debt before buying a house.

Just remember to consider the monthly student loan payments and your homeowner costs. Multiple loan payments add up quickly.

It's not necessarily harder to buy a house as student loan borrowers.

But regular student loan payments with regular mortgage payments can be expensive, so be careful to stay on top of your payments.

Student loan payment assistance programs may help with federal student loans, such as income-driven repayment plans. So explore all your options if you run into a hardship.

Welcome to my website, your number one source for real estate information! As a lifelong resident of Massachusetts, I can help you with the best areas for your individual needs. I know the towns with train lines, commuter rails and easy access to highways. As a mother of three and a child of teachers, I know the importance of quality education. I am well aware of the towns with the highest rated public schools systems and know the best private schools in the area as well.